Consolidated financial statements of a group of companies are prepared on the basis of single economic entity concept.

Definition

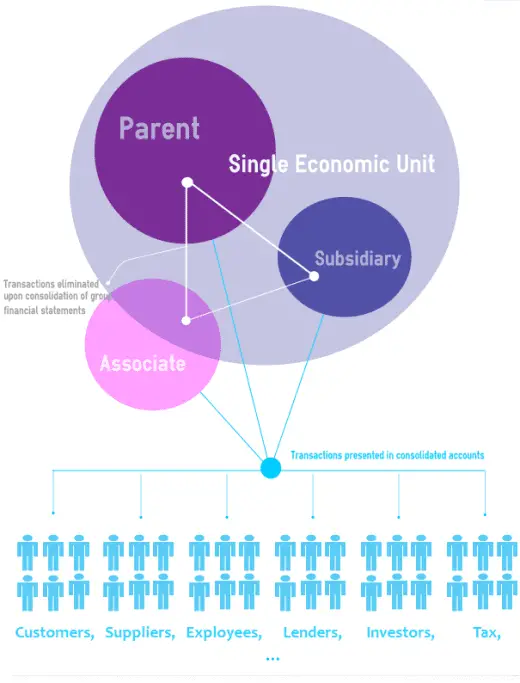

Single Economic Entity Concept suggests that companies associated with each other through the virtue of common control operate as a single economic unit and therefore the consolidated financial statements of a group of companies should reflect the essence of such arrangement.

Explanation

Consolidated financial statements of a group of companies must be prepared as if the entire group constitutes a single entity in order to avoid the misrepresentation of the scale of group’s activities.

It is therefore necessary to eliminate the effects of any inter-company transactions and balances during the consolidation of group accounts such as the following:

- Inter-company sales and purchases.

- Inter-company payables and receivables.

- Inter-company payments such as dividends, royalties & head office charges.

Inter-company transactions must be eliminated as if the transactions had not occurred in the first place. Examples of adjustments that may be required to eliminate the effects of inter-company transactions include:

- Elimination of unrealized profit or loss on the sale of assets member companies of a group.

- Elimination of excess or deficit depreciation expense in respect of a fixed asset purchased from a member company at a price that was higher or lower than the net book value of the asset in the books of the seller.

Example

XYZ PLC is a company specializing in the manufacturing of fertilizers. At the start of the current accounting period, XYZ PLC acquired DEF PLC, a chemicals producer.

Following is a summary of the financial results of the two companies during the year:

| XYZ | DEF | |

|---|---|---|

|

Sales |

120 |

50 |

|

Cost of sales |

60 |

20 |

|

Gross profit |

60 |

30 |

|

Operating expenses |

20 |

10 |

|

Net profit |

40 |

20 |

XYZ PLC purchased chemicals worth $20m from DEF PLC which it used in the manufacture of fertilizers sold during the year.

Consolidation of XYZ Group’s financial results will require an adjustment in respect of the inter-company sale and purchase in order to conform to the single entity principle.

Consolidated financial results of the two companies will be presented as follows:

| XYZ Group | ||

|---|---|---|

|

Sales |

(120 + 50 - 20) |

150 |

|

Cost of sales |

(60 + 20 - 20) |

60 |

|

Gross profit |

90 |

|

|

Operating expenses |

(20 + 10) |

30 |

|

Net profit |

60 |

|

Since XYZ Group, considered as a single entity, cannot sell and purchase to itself, the sales and purchases in the consolidated income statement have been reduced by $20 m each in order to present the sales and purchases with external customers and suppliers.

If we ignore the single entity concept, XYZ Group’s financial results will present sales of $170 m and cost of sales amounting $80 m. Although the net profit of the group will be unaffected by the inter-company transaction, the size of the Group’s operations will be misrepresented due to the overstatement.

Summary

Following diagram summarizes the implications of the single entity principle on group financial reporting.

Quiz

How much do you know about single economic entity principle?

Take the free quiz below and find out!

Question

ABC Motors PLC is a leading cars manufacturer with presence in several countries through its network of subsidiaries and associates.

ABC Motors PLC is in the process of preparation of its consolidated financial statements.

Which of the following transactions and events should be reflected in ABC Motors Group’s consolidated financial statements?

Management consultancy charges received by ABC Motors PLC from its subsidiaries.

Incorrect.

ABC Motors Group cannot present income and expense in respect of the consultancy fee charged to a member of the Group in the consolidated accounts.

ABC Motors PLC may however report income in respect of the consultancy fee in its separate financial statements.

Payment of dividend by ABC Motors PLC to its shareholders.

Correct.

Shareholders of ABC Motors PLC should be considered as separate from the Group and hence transactions with shareholders (e.g. dividends) must be reported in the consolidated financial statements.

Purchase of equipment from a subsidiary at fair value.

Incorrect.

Transactions of a parent with subsidiary, irrespective of whether they are executed on an arm's length basis or not, should not be reflected in the consolidated financial statements.

Consequently, the effects of the purchase transaction must be eliminated from the group accounts as if the transaction did not take place.

Related party disclosure of the inter-company transactions between ABC Motors PLC and its subsidiaries.

Incorrect.

For the purpose of consolidated financial statements of the Group, related party transactions should only be disclosed in respect of entities outside the Group.

Inter-company transactions between member companies of a group may however be disclosed in their separate financial statements.