Explanation

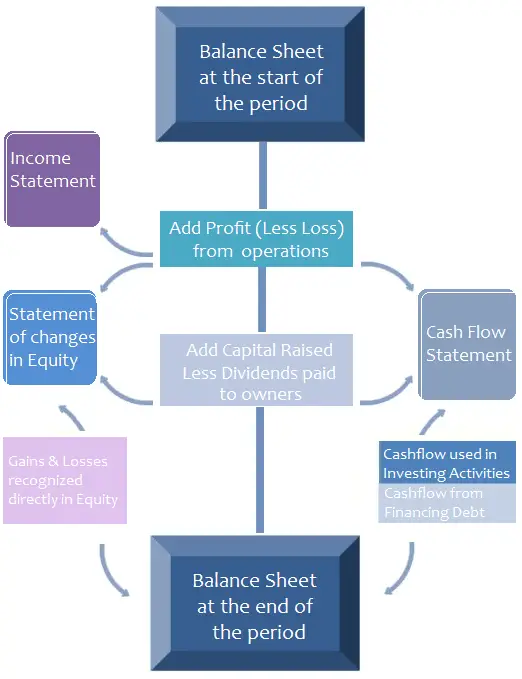

Financial Statements reflect the effects of business transactions and events on the entity. The different types of financial statements are not isolated from one another but are closely related to one another as is illustrated in the following diagram.

Balance Sheet

Balance Sheet, or Statement of Financial Position, is directly related to the income statement, cash flow statement and statement of changes in equity.

Assets, liabilities and equity balances reported in the Balance Sheet at the period end consist of:

- Balances at the start of the period;

- The increase (or decrease) in net assets as a result of the net profit (or loss) reported in the income statement.

- The increase (or decrease) in net assets as a result of the net gains (or losses) recognized outside the income statement and directly in the statement of changes in equity (e.g. revaluation surplus).

- The increase in net assets and equity arising from the issue of share capital as reported in the statement of changes in equity.

- The decrease in net assets and equity arising from the payment of dividends as presented in the statement of changes in equity.

- The change in composition of balances arising from inter balance sheet transactions not included above (e.g. purchase of fixed assets, receipt of bank loan, etc).

- Accruals and Prepayments.

- Receivables and Payables.

Income Statement

Income Statement, or Profit and Loss Statement, is directly linked to balance sheet, cash flow statement and statement of changes in equity.

The increase or decrease in net assets of an entity arising from the profit or loss reported in the income statement is incorporated in the balances reported in the balance sheet at the period end.

The profit and loss recognized in income statement is included in the cash flow statement under the segment of cash flows from operation after adjustment of non-cash transactions. Net profit or loss during the year is also presented in the statement of changes in equity.

Statement of Changes in Equity

Statement of Changes in Equity is directly related to balance sheet and income statement.

Statement of changes in equity shows the movement in equity reserves as reported in the entity’s balance sheet at the start of the period and the end of the period. The statement therefore includes the change in equity reserves arising from share capital issues and redemption, the payments of dividends, net profit or loss reported in the income statement along with any gains or losses recognized directly in equity (e.g. revaluation surplus).

Cash Flow Statement

Statement of Cash Flows is primarily linked to balance sheet as it explains the effects of change in cash and cash equivalents balance at the beginning and end of the reporting period in terms of the cash flow impact of changes in the components of balance sheet including assets, liabilities and equity reserves.

Cash flow statement therefore reflects the increase or decrease in cash flow arising from:

- Change in share capital reserves arising from share capital issues and redemption.

- Change in retained earnings as a result of net profit or loss recognized in the income statement (after adjusting non-cash items) and dividend payments.

- Change in long term loans due to receipt or repayment of loans.

- Working capital changes as reflected in the increase or decrease in net current assets recognized in the balance sheet.

- Change in non current assets due to receipts and payments upon the acquisitions and disposals of assets (i.e. investing activities).