Definition

Fixed Overhead Total Variance is the difference between actual and absorbed fixed production overheads during a period.

Formula

Fixed Overhead Total Variance:

|

= |

Actual Fixed Overheads |

x |

Absorbed Fixed Overheads

|

|

= |

Actual Fixed Overheads |

x |

Actual Output x Fixed Overhead Absorption Rate |

Example

Motors PLC is a manufacturing company involved in the production of automobiles.

Information from its last budget period is as follows:

|

Actual Production |

275,000 units |

|

Budgeted Production |

250,000 units |

|

Actual Fixed Production Overheads |

$526,000,000 |

|

Budgeted Fixed Production Overheads |

$500,000,000 |

Calculate the fixed overhead total variance.

In order to calculate the required variance, we first need to find out the standard absorption rate:

|

Fixed Overhead Absorption Rate |

= |

budgeted fixed overheads |

|

budgeted output |

||

|

|

= |

$50,000,000 |

|

250,000 units |

||

|

|

= |

$2,000 per unit |

Now we can apply the formula to calculate the fixed overhead total variance as follows:

| = | Actual Fixed Overheads | - | Absorbed Fixed Overheads |

|---|---|---|---|

|

|

|

|

|

|

= |

$526,000,000 |

- |

275,000 x $2,000 |

|

= |

$526,000,000 |

- |

$550,000,000 |

|

= |

$24,000,000 Favorable |

||

The variance is favorable because the actual expense is lower than the fixed overheads absorbed during the period.

Explanation

Fixed Overhead Total Variance is the difference between the actual fixed production overheads incurred during a period and the ‘flexed’ cost (i.e. fixed overheads absorbed).

In case of absorption costing, the fixed overhead total variance comprises the following sub-variances:

- Fixed Overhead Expenditure Variance: the difference between actual and budgeted fixed production overheads.

- Fixed Overhead Volume Variance: the difference between fixed production overheads absorbed (flexed cost) and the budgeted overheads.

Under marginal costing system, fixed production overheads are not absorbed in the cost of output. Fixed overhead total variance in such instance will therefore equal to the fixed overhead expenditure variance because the budgeted and flexed overhead cost shall be the same.

Example

Continuing the Motors PLC example above, we have the following information:

|

Actual Production |

275,000 units |

|

Budgeted Production |

250,000 units |

|

Actual Fixed Production Overheads |

$526,000,000 |

|

Budgeted Fixed Production Overheads |

$500,000,000 |

Calculate the fixed overhead volume variance and fixed overhead expenditure variance.

| Fixed Overhead Expenditure Variance | |

|---|---|

|

Actual Production |

$526,000,000 |

|

Less: Budgeted Fixed Overheads |

$500,000,000 |

|

Variance |

$26,000,000 |

The variance is adverse because Motors PLC incurred greater expense than provided for in the budget.

| Fixed Overhead Volume Variance | |

|---|---|

|

Budgeted Production |

$500,000,000 |

|

Less: Absorbed Fixed Overheads [above example] |

$550,000,000 |

|

Variance |

$50,000,000 |

The variance is favorable because Motors PLC yielded a higher output than anticipated in the budget.

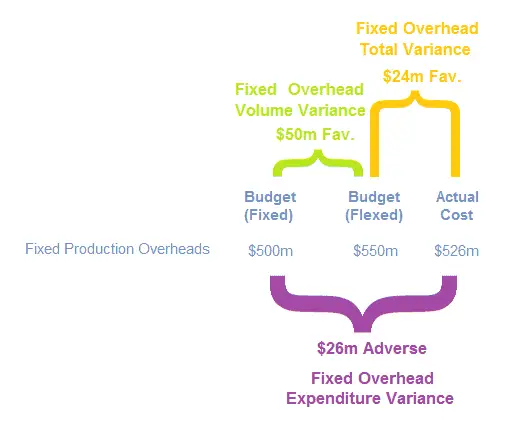

Proof Check

The sum of fixed overhead expenditure and volume variances should equal to the fixed overhead total variance as calculated in above Example:

|

Fixed Overhead Expenditure Variance |

$ 26,000,000 |

Adverse |

|

Fixed Overhead Volume Variance |

$ 50,000,000 |

Favorable |

|

Total |

$ 24,000,000 |

Favorable |

|

Fixed Overhead Total Variance |

$ 24,000,000 |

Favorable |

The variance is favorable because Motors PLC yielded a higher output than anticipated in the budget.

The following diagram summarizes the breakup of the total variance into its sub-components: