Relevant cost of labor is the incremental and avoidable cost of labor that is incurred as a consequence of a business decision.

Direct Labor

Direct labor includes personnel that are directly involved in the production process (e.g. assembly line workers).

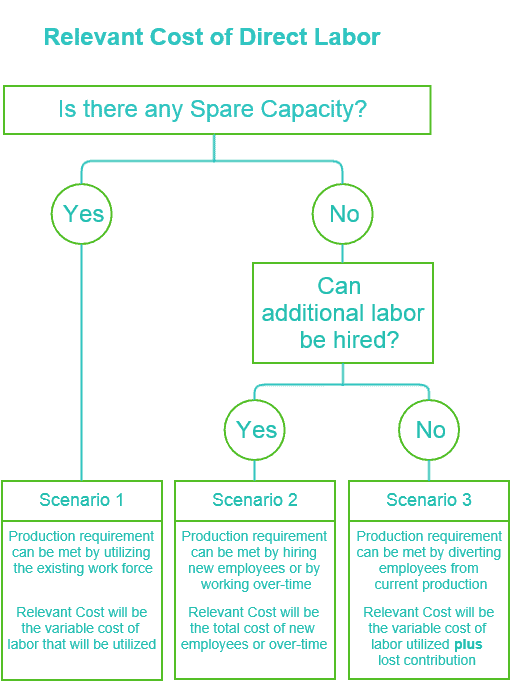

Relevant cost of direct labor depends on how the labor requirements of a proposed business action are planned to be met.

The following diagram summarizes the impact of different scenarios on the relevant cost of direct labor:

Scenario 1: Availability of spare capacity

This is applicable where the labor hours available exceed the labor hours currently being utilized, i.e. spare capacity exists.

Where spare capacity is available, relevant cost is the incremental cost of utilizing additional labor hours, i.e. variable cost of each additional hour.

Fixed costs which do not change as a result of the change in labor hours consumed should not be considered as relevant. For instance, if direct labor is guaranteed idle time pay equal to 60% of the normal pay during periods of lower demand, the relevant cost of labor shall be only 40% of the normal pay because 60% of the cost will be incurred irrespective of any additional work undertaken.

Scenario 2: Overtime and Additional Staff

When existing labor is already being fully utilized, any additional labor requirement may be met either by offering overtime to current staff or by hiring new employees.

The relevant cost of direct labor in this scenario shall be the total cost of additional labor hours required for the proposed business action.

Scenario 3: Divert Labor Resources

As a last preference, direct labor engaged in current production may be diverted towards the new business proposition where no spare capacity exists and neither can new labor be hired externally.

The relevant cost of direct labor in this scenario shall be the variable cost of labor to be utilized plus any loss of contribution resulting from the discontinuation of current production activities. The lost contribution represents the opportunity cost of using labor on a new project when current production has to be sacrificed.

Indirect Labor

Indirect labor consists of employees that are not directly involved in the production such as managerial and administrative staff.

Relevant cost of indirect labor is the incremental cost, i.e. the additional cost that results directly from the implementation of the proposed business action.

Unlike direct labor, the cost of indirect labor is largely fixed and unaffected by variations in output in the short term in most cases because managerial and administrative staff is usually salaried. Therefore, for very short term decisions (e.g. pricing decisions of special orders), the relevant cost of indirect labor would often be negligible.

Example

The Guitar Company (TGC) is a small company specializing in the manufacture of hand-made acoustic guitars.

TGC has received a request to submit their price quote for the supply of 50 custom made acoustic guitars. TGC has a policy of pricing custom orders at a markup of 50% above their relevant cost.

Detail and relevant cost of labor that will be utilized on the order is as follows:

| Labor | Detail | Relevant cost | Explanation |

|---|---|---|---|

|

Liza |

This represents the estimated time that will be spent on the order by the procurement manager Liza on the purchase of tools and materials for the order. |

- |

Since Liza's salary cost is fixed and does not increase as a result of this order, her relevant cost is nil. |

|

Michael |

Designing and cutting of guitars will be done by Michael. |

$2,000 |

(200 hours x $10) |

|

Sam |

Gluing & binding of guitar parts is usually done by Sam who is paid $13 per hour. Sam however will only be able to work 100 out of the 250 hours required for this order due to his commitment on other orders. |

$1,300 |

(100 hours x $13) |

|

Bob |

The remaining 150 hours required for gluing and binding of guitars will need to be contracted to Bob who has agreed to work for TGC on a 3-months contract for a fixed fee of $500 plus $15 per hour of work. |

$2,250 (variable) |

(150 hours x $15) |

|

Smith |

Smith is responsible for shaping the guitars. He is paid $15 per hour of work. |

$2,250 (variable cost) |

(150 hours x $15) |

|

Bob |

Gibson handles the finishing of guitars. |

$1,000 |

(100 hours x $10) |