Relevant cost of materials is the incremental future cost of utilizing materials in a proposed business decision. The past cost that has already been incurred on acquisition of materials is not relevant because it constitutes a sunk cost.

Summary

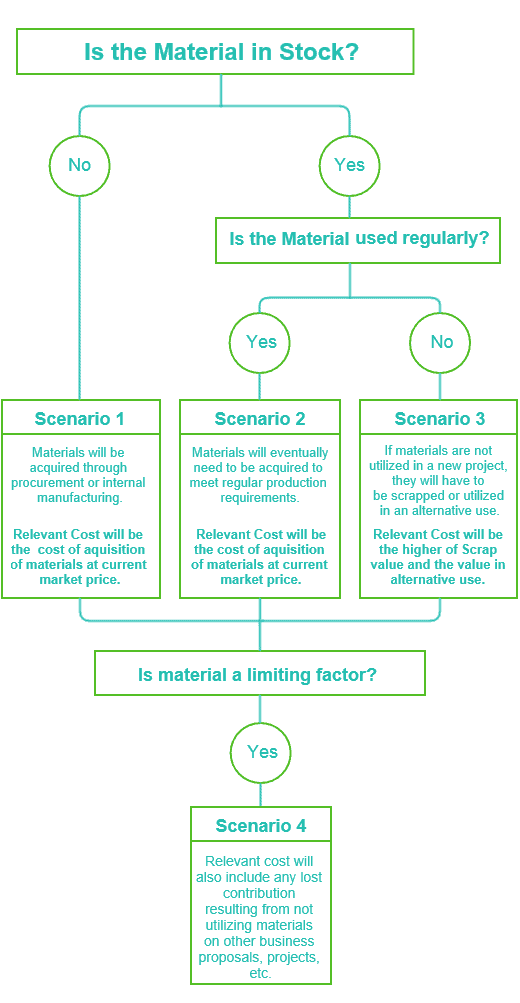

The following diagram summarizes how to calculate the relevant cost of materials in different situations. The same principles can be applied in case of both direct and indirect materials.

Scenario 1: Out of Stock

If the required material is not available in stock, the relevant cost will be the current or expected cost of purchase.

In case of businesses that are backwards-integrated (e.g. an oil refinery having direct access to oil reserves), there may be an option to source the required materials internally rather than procuring externally. In such case, the relevant cost will be the lower of current market price of the materials if purchased externally and the incremental cost of acquiring materials internally. This concept will be covered in detail in the topic: Make or Buy Decisions.

Scenario 2: In Stock, Regular Use

Even if the required material is available in stock, the relevant cost shall equal to the current cost of purchase if the material is used regularly in a business. This is because the consumption of the current stock of materials, in for example, a new project will necessitate the purchase of more stock at the current market price to meet other production needs (i.e. the consumption of materials will ultimately cost the business the current market rate of materials).

Scenario 3: In Stock, No Regular Use

If a material is available in stock but is not used regularly in production, the relevant cost shall be the opportunity cost of using the material in the proposed business action instead of selling it or utilizing it in an alternative use (e.g. as a substitute material).

Relevant cost in this case shall be the higher of:

- Scrap value (disposal value); and

- Value in alternative use.

The relevant cost as calculated above should not however exceed the current market value of materials unless they are in short supply (see scenario 4 below).

Scenario 4: Limiting Factor

Where material is in short supply and its usage will restrict other production activities (i.e. material is a limiting factor), the relevant cost of materials (in addition to the relevant cost calculated in the scenarios above) will also include the loss of contribution resulting from the inability to engage in other production activities. The loss of contribution represents the opportunity cost of using the scarce material resource on the new business proposition instead of utilizing it to pursue the next best production alternative.

Example

The Guitar Company (TGC) is a small company specializing in the manufacture of hand-made acoustic guitars.

TGC has received a request to submit their price quote for the supply of 50 custom made acoustic guitars. TGC has a policy of pricing custom orders at a markup of 50% above their relevant cost.

Most materials required for the order will be provided by the customer. The details and relevant cost of other materials to be sourced by TGC are as follows:

| Materials | Detail | Relevant cost | Explanation |

|---|---|---|---|

|

Rosewood |

TGC currently has no quantity of rosewood in stock and would have to purchase it at the cost of $150 per sheet. |

$15,000 |

(100 x $150) = $15,000 |

|

Strings |

Silk and steel guitar strings will be used on the order. |

$50 |

Relevant cost is the scrap value as the strings have no value in alternative use. The past cost of $10 per string set is a sunk cost and therefore not relevant. |

|

Glue |

Glue required for the order is available in stock. The glue was purchased 3 month ago at a cost $10 per liter. |

$150 |

(10 x $15) |