Make-or-buy decisions involve the assessment of whether an organization should continue manufacturing a product or service ‘in-house’, or if it should just buy those from an outside supplier.

Why Outsource?

If an organization is already manufacturing the entire product internally without involving any outside contractor, why should it outsource any of its business processes?

Outsourcing can improve the profitability of businesses by:

- Enabling businesses to focus on their core products by delegating non-critical processes to external organizations;

- Benefiting from a lower cost offered by outside suppliers that are more efficient in producing certain products or services;

- Overcoming production constraints caused by a shortage of internal resources;

- Procuring products and services of a higher quality.

Qualitative Analysis

Organizations need to weigh the short-term financial impact of outsourcing against the long term consequences.

Several factors influence make-or-buy decisions.

- Quality

- Will external sourcing compromise the quality of the final product?

- Can a business enhance the quality of its products by hiring a specialist?

- Reliability:

- Is an external supplier better equipped to deal with sudden fluctuations in production requirements?

- Will delegating the supply of a business process make it vulnerable to supply dips?

- Control:

- How important is a specific process, product, or component, to the core business?

- Will giving up the control of a process make the business less flexible?

- Capacity

- How will the organization deal with idle resources if it decides against manufacturing in-house?

- Will outsourcing cause redundancies and how will they impact the organization?

- Competitiveness

- How will outsourcing affect the profitability of business?

- Is the cost of buying a component or process from outside lower than the internal production cost?

- Can outsourcing help the business improve its competitiveness by channeling its focus to the key areas?

Quantitative Analysis

Make-or-buy decisions must be based on the relevant cost of each option.

Relevant costs in make-or-buy decisions include all incremental cash flows.

Any cost that does not change as a result of the decision should be ignored such as depreciation and indirect fixed costs.

Calculating the relevant cost is the first step in finding the most cost-effective option.

Following are examples of relevant costs in make-or-buy decision

| Relevant Costs | Examples |

|---|---|

|

Variable costs |

|

|

Direct fixed costs |

|

|

Opportunity cost |

|

Examples of irrelevant costs in make-or-buy decisions are as follows:

| Non-Relevant Costs | Examples |

|---|---|

|

Indirect fixed costs |

|

|

Non-cash expenses |

|

|

Sunk costs |

|

|

Committed costs |

|

Once we sort out the relevant costs in the make-or-buy decision, we need to find which option minimizes the total cost.

The approach to finding the optimum solution in an outsourcing problem depends on the number of limiting factors.

| Number of limiting factors | Make or Buy? |

|---|---|

|

0 |

Compare the relevant cost of in-house production with the cost of acquiring product or service externally. |

|

1 |

If the internal cost exceeds the external price, it is better to buy. |

|

≥2 |

The optimum solution can be found by using linear programming. |

Example

Phone Inc. is a manufacturer of cell phones. Until now the company has manufactured all phone accessories in-house.

The company CFO is wondering if it can reduce the manufacturing cost of cell phones by outsourcing the production of 3 accessories: charger, battery, and earphone.

The accountant has forecast the following information for the next year.

| Charger | Battery | Earphone | |

|---|---|---|---|

|

Sales (Units) |

10,000 |

10,000 |

10,000 |

|

Labor hours / unit |

0.5 |

0.25 |

0.2 |

|

Machine hours / unit |

0.10 |

0.15 |

0.12 |

|

Cost of Production |

$ |

$ |

$ |

|

Variable cost |

|

|

|

|

Direct labor |

20,000 |

30,000 |

40,000 |

|

Direct materials |

10,000 |

20,000 |

30,000 |

|

Variable overheads |

10,000 |

10,000 |

10,000 |

|

Fixed cost |

|

|

|

|

Direct fixed cost |

|

|

|

|

Depreciation |

10,000 |

10,000 |

20,000 |

|

Salaries |

20,000 |

10,000 |

10,000 |

|

Rent |

10,000 |

20,000 |

20,000 |

|

Indirect fixed cost |

|

|

|

|

Non-manufacturing overheads |

10,000 |

20,000 |

30,000 |

|

Total cost |

100,000 |

80,000 |

120,000 |

Direct fixed costs relate specifically to each component. Non-manufacturing overheads represent the allocated share of head office expenses.

Outsource Inc. has supplied the following quotation for the supply of the three components.

| Charger | Battery | Earphone | |

|---|---|---|---|

|

Sales (Units) |

$ |

$ |

$ |

|

Price |

10 |

4 |

8 |

Based on quantitative analysis:

A. How many units of each component should be outsourced?

B. If only 3,000 labor hours are available, how many units of each component should be produced internally or outsourced?

C. If only 3,000 labor hours and 1,000 machine hours are available, how many units of each component shall be manufactured or outsourced?

Solution

A. To find the optimum solution, we need to compare the relevant cost of making each component with the buying price.

| Charger | Battery | Earphone | |

|---|---|---|---|

|

|

$ |

$ |

$ |

|

Total cost |

100,000 |

80,000 |

120,000 |

|

Less: Non-Relevant Costs |

|

|

|

|

Depreciation |

10,000 |

10,000 |

20,000 |

|

Non-manufacturing overheads |

10,000 |

20,000 |

30,000 |

|

Relevant cost |

80,000 |

50,000 |

70,000 |

|

Units |

10,000 |

10,000 |

10,000 |

|

Relevant Cost per Unit |

8 |

5 |

7 |

|

Acquisition Price |

10 |

4 |

8 |

|

Incremental cost of buying |

2 |

(1) |

1 |

|

Make or Buy |

Make |

Buy |

Make |

|

Units |

10,000 |

10,000 |

10,000 |

As the internal cost of making batteries exceeds the external price of buying, it is beneficial to outsource their production entirely. Chargers and earphones will be produced internally to minimize cost.

B. We need to rank the three components for production priority based on the incremental cost per limiting factor.

Batteries are excluded from the calculation of production priority because they will be outsourced anyway based on our assessment in Part A.

| Charger | Earphone | |

|---|---|---|

|

Calculation of Production Priority |

$ |

$ |

|

Incremental saving from internal manufacturing |

2 |

1 |

|

Labor hours per unit |

0.5 |

0.2 |

|

Incremental saving Per unit of limiting factor |

4 |

5 |

|

Production rank |

2 |

1 |

Self-production of earphones result in higher savings per labor hour compared to chargers which rank them higher in the production priority.

Phone Inc. should use labor hours in the production of maximum units of earphones and manufacture chargers only if any surplus labor hours are available.

| Component | Hours | Earphone | ||

|---|---|---|---|---|

|

Earphone |

(10,000 units × 0.2) |

2,000 |

|

10,000 |

|

Charger |

(3000 hours – 2000) |

1,000 |

(1000 / 0.5) |

2,000 |

|

Total |

|

3,000 |

|

|

Once we have calculated the self-manufactured units of each accessory, we can calculate the number of units we need to outsource as the balancing figure.

| Units | Charger | Battery | Earphone |

|---|---|---|---|

|

Make |

2,000 |

0 |

10,000 |

|

Buy |

8,000 |

10,000 |

0 |

|

Total |

10,000 |

10,000 |

10,000 |

C. We are going to solve this part of the problem by using the Simplex Method of linear programming because it involves multiple constraints and products. If you are unfamiliar with the basics of linear programming, I suggest you review this lesson.

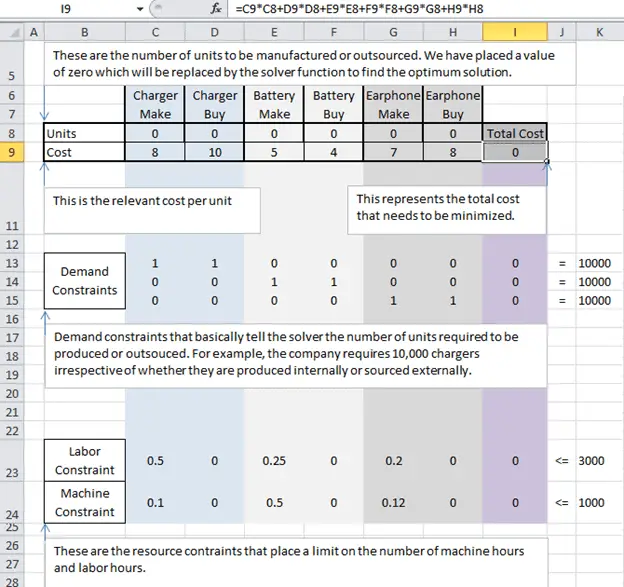

To solve this problem, we first we need to define the objective function and enter data relating to the cost and constraints for each accessory in Microsoft Excel.

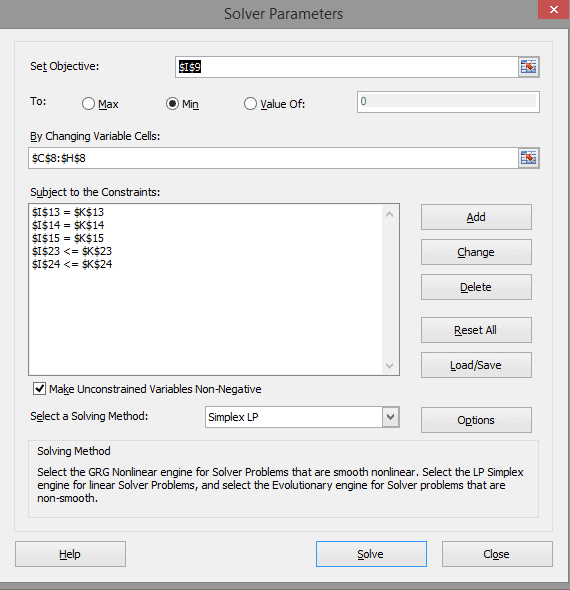

We then use the Solver function to mark the relevant data as follows:

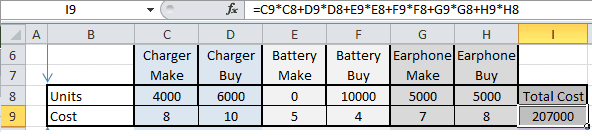

Pressing the Solve button will return you the optimum solution:

We cannot cover all aspects of the Simplex Method in this article as the topic deserves a video tutorial of its own which I will be adding soon.

Do subscribe to our YouTube channel to catch any updates. Let us know if you have any questions on this topic in the comments below.